Pension Plan Updates 2026: Defined Benefit for Secure Retirement

Navigating the complex landscape of Pension Plan Updates 2026 is crucial for understanding your defined benefit options and ensuring a secure and stable retirement in the evolving financial environment.

As we approach 2026, understanding the significant Pension Plan Updates 2026 is paramount for anyone relying on a defined benefit plan for their retirement. These changes can profoundly impact your financial future, making informed decision-making more critical than ever.

Understanding Defined Benefit Plans in 2026

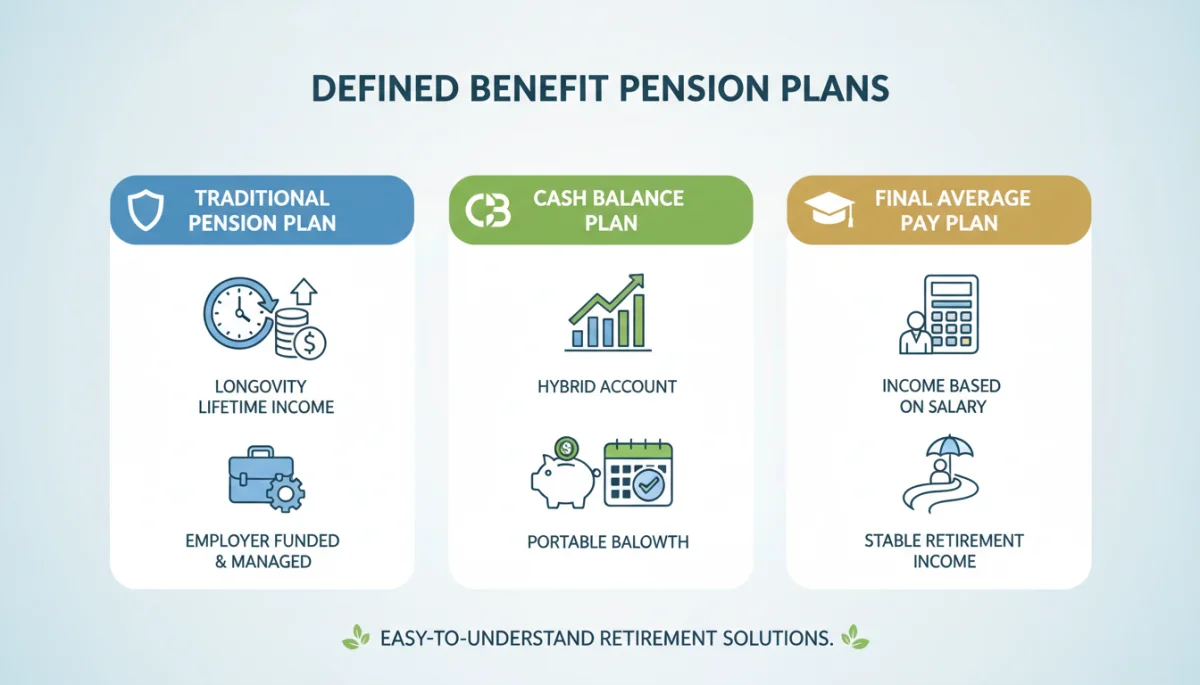

Defined benefit pension plans, often seen as a cornerstone of retirement security, promise a specified monthly benefit at retirement. This contrasts sharply with defined contribution plans, where the retirement income depends on investment performance. In 2026, these traditional plans are undergoing significant adjustments, driven by economic shifts, regulatory changes, and evolving demographic trends. For many, a defined benefit plan represents a critical safety net, providing predictable income that can weather market volatility.

The stability offered by defined benefit plans is a key attraction, especially for those seeking financial predictability in their later years. However, this stability comes with its own set of complexities, particularly as plan administrators adapt to new mandates and economic realities. Staying informed about these changes is not just a recommendation; it’s a necessity for safeguarding your retirement income.

Current Landscape and Future Projections

The year 2026 brings new projections for defined benefit plans. Actuarial assumptions are being refined, and interest rate environments continue to influence funding levels. This means that while your core benefit might remain, the underlying mechanisms supporting it are constantly being re-evaluated.

- Increased scrutiny on plan solvency and funding ratios.

- Potential adjustments to cost-of-living allowances (COLAs).

- Emphasis on sustainable benefit payouts over longer lifespans.

Understanding these projections helps beneficiaries anticipate potential shifts in their retirement income. It also empowers them to engage with their plan administrators or financial advisors regarding their specific situation. The future of defined benefit plans is one of adaptation and resilience, aiming to balance promises made with financial prudence.

In essence, defined benefit plans in 2026 remain a vital component of many retirement strategies. However, beneficiaries must actively monitor their plan’s health and any communications from their administrators. This proactive approach ensures that the promised security truly materializes when needed most.

Key Regulatory Changes Impacting Pensions

The regulatory environment surrounding pension plans is a dynamic one, and 2026 introduces several key changes designed to enhance security and sustainability. These updates often stem from legislative efforts to protect retirees, ensure proper funding, and adapt to economic realities. Understanding these regulations is crucial for both plan sponsors and beneficiaries, as they can directly influence benefit structures and payouts.

These regulatory shifts are not merely bureaucratic hurdles; they are fundamental safeguards. They aim to prevent underfunding, improve transparency, and ensure that pension promises can be met for decades to come. While complex, their intent is to strengthen the bedrock of retirement security.

New Legislation and Compliance Standards

Expect new federal guidelines in 2026 focusing on stricter funding requirements and enhanced reporting. These measures are designed to provide greater oversight and reduce the risk of plan insolvency. Employers sponsoring defined benefit plans will face increased compliance burdens, which in turn should lead to more robustly funded plans.

- Mandatory annual actuarial certifications.

- Improved disclosure requirements for plan financial health.

- Penalties for consistent underfunding.

These compliance standards represent a commitment to safeguarding pension assets. They serve as a critical check on plan management, ensuring that decisions are made with the long-term interests of beneficiaries in mind. For retirees, this translates to greater peace of mind regarding the stability of their future income.

Furthermore, state-level regulations may also emerge, complementing federal initiatives. It is important to remember that pension plans operate within a layered regulatory framework, and changes at any level can have ripple effects. Staying informed about both federal and state legislative developments is therefore essential for comprehensive understanding.

Impact of Economic Trends on Defined Benefit Payouts

The broader economic landscape plays a significant role in the health and payout capacity of defined benefit pension plans. Factors such as inflation, interest rates, and investment market performance directly influence a plan’s ability to meet its obligations. In 2026, these economic trends continue to present both opportunities and challenges for pension administrators and beneficiaries alike.

Pension plans are long-term financial commitments, making them particularly sensitive to sustained economic shifts. Understanding how these macro-economic forces interact with your pension plan can provide valuable insights into its long-term viability and the potential for benefit adjustments.

Inflation and Purchasing Power

Rising inflation, a persistent concern, directly erodes the purchasing power of fixed pension incomes. While some defined benefit plans offer cost-of-living adjustments (COLAs), these may not always keep pace with actual inflation rates. Beneficiaries must consider the real value of their pension over time, not just the nominal amount.

- Evaluating COLA provisions in your specific plan.

- Understanding the impact of sustained inflation on retirement budgets.

- Exploring supplementary income strategies to mitigate inflation’s effects.

The challenge of inflation highlights the importance of diversified retirement planning. Relying solely on a fixed pension without accounting for inflationary pressures can lead to a gradual reduction in living standards. Proactive financial planning, including investments that offer inflation protection, can be a valuable strategy.

Interest Rates and Investment Returns

Low interest rates can pose a challenge for pension funds, as they often rely on fixed-income investments to generate returns. Conversely, higher interest rates can improve a plan’s funding status. Investment market volatility also impacts the asset base of a pension fund. Administrators must navigate these market dynamics carefully to ensure long-term solvency.

The interplay between interest rates and investment returns is a delicate balance. Pension fund managers employ sophisticated strategies to optimize returns while managing risk. Beneficiaries should be aware that their plan’s financial health is intrinsically linked to the performance of these managed assets.

Strategies for Maximizing Your Defined Benefit

While external factors and regulatory changes influence defined benefit plans, there are proactive steps beneficiaries can take to maximize their benefits and ensure a more secure retirement. These strategies involve understanding your plan’s specifics, making informed decisions at critical junctures, and integrating your pension with your broader financial plan.

Taking control of what you can is key. Even with a defined benefit plan, personal financial decisions can significantly enhance the value and impact of your pension throughout your retirement years.

Understanding Your Plan Documents

The first step is to thoroughly review your Summary Plan Description (SPD) and other plan documents. These documents outline your eligibility, benefit calculation formula, vesting schedule, and payout options. Pay close attention to details regarding early retirement provisions, survivor benefits, and any potential for benefit reductions.

- Requesting an updated SPD from your plan administrator.

- Clarifying any ambiguous clauses with a plan representative.

- Keeping accurate records of your service history and contributions.

A deep understanding of your plan documents empowers you to make the best decisions. It helps you identify potential pitfalls and opportunities, ensuring you don’t leave any entitled benefits on the table. Knowledge is truly power when it comes to retirement planning.

Choosing the Right Payout Option

Most defined benefit plans offer various payout options, such as a single life annuity, joint and survivor annuity, or even a lump sum distribution in some cases. Each option has different implications for the amount you receive, tax treatment, and provisions for your spouse or beneficiaries. Carefully consider your personal circumstances, health, and family needs before making a choice.

This decision is often irreversible, making it one of the most critical choices in your retirement journey. Consulting with a financial advisor who specializes in retirement planning can provide invaluable guidance in selecting the option that best aligns with your long-term goals and risk tolerance.

The Role of Financial Advisors in Pension Planning

Navigating the complexities of Pension Plan Updates 2026 and making optimal decisions regarding your defined benefit options can be daunting. This is where the expertise of a qualified financial advisor becomes invaluable. Their role extends beyond simple investment advice to encompass comprehensive retirement planning, integrating your pension with all other financial assets and liabilities.

A good financial advisor acts as a guide, helping you translate intricate plan documents and economic forecasts into actionable strategies tailored to your unique situation. Their objective perspective can be crucial in making emotionally charged decisions about your retirement income.

Expert Guidance on Payout Choices

As discussed, choosing a pension payout option is a significant decision. An advisor can help you analyze the pros and cons of single life vs. joint and survivor annuities, considering your life expectancy, your spouse’s needs, and your overall financial picture. They can also help evaluate the implications of a lump sum distribution versus monthly payments, particularly regarding tax consequences and investment management.

- Analyzing your specific plan’s payout options and their tax implications.

- Projecting future income needs based on your lifestyle and health.

- Developing a diversified income strategy that includes your pension.

Their expertise ensures that your chosen payout strategy aligns perfectly with your broader retirement goals, providing clarity and confidence in a decision that will impact the rest of your life.

Integrating Pension with Holistic Financial Planning

A defined benefit pension is just one piece of your financial puzzle. A comprehensive financial advisor will help you integrate your pension income with Social Security benefits, personal savings, investments, and any other income sources. This holistic approach ensures that all components work together to create a robust and sustainable retirement income stream.

They can also provide guidance on estate planning, healthcare costs in retirement, and managing unexpected financial events. By viewing your pension within this larger context, you can achieve greater financial resilience and peace of mind. The goal is not just to receive your pension, but to make it work optimally within your entire financial ecosystem.

Future Outlook for Defined Benefit Plans Post-2026

Looking beyond 2026, the trajectory of defined benefit pension plans continues to evolve. While some employers have shifted towards defined contribution models, many legacy plans remain, and their long-term sustainability is a constant focus. The future promises continued adaptation, driven by demographic shifts, economic performance, and regulatory refinements. Understanding these potential future trends allows for even more proactive retirement planning.

The landscape of retirement benefits is never static. Defined benefit plans, with their inherent promises, face ongoing pressures to remain solvent and relevant. Beneficiaries should maintain a forward-looking perspective, anticipating changes rather than reacting to them.

Longevity Risk and Funding Solutions

One of the primary challenges for defined benefit plans is longevity risk – the increasing lifespan of retirees. This means plans must pay out benefits for longer periods than initially projected. In response, we may see more innovative funding solutions and risk transfer strategies emerging post-2026, such as pension risk transfers (PRTs) to insurance companies.

- Increased use of actuarial science to refine longevity assumptions.

- Exploration of pooled employer plans (PEPs) for smaller employers.

- Focus on robust investment strategies to meet long-term liabilities.

These solutions aim to bolster the financial health of pension plans, ensuring that the promise of a secure retirement can be maintained for future generations of retirees. While complex, these innovations are critical for the long-term viability of defined benefit structures.

Shifting Employer Sponsorship and Hybrid Models

While new defined benefit plans are rare, existing ones continue to be managed. Some employers might explore hybrid models that combine elements of defined benefit and defined contribution plans, offering a blend of predictability and flexibility. This could involve cash balance plans or other innovative designs that aim to balance employer costs with employee security.

The trend towards hybrid models reflects an ongoing effort to find sustainable and attractive retirement solutions. For beneficiaries, it means a continued need to understand the specifics of their plan, as these models can vary significantly in their structure and benefits. The future of defined benefit plans is one of cautious optimism and continuous innovation, striving to deliver on their fundamental promise of retirement security.

| Key Aspect | Brief Description |

|---|---|

| Regulatory Changes | Stricter funding rules and enhanced reporting for plan solvency in 2026. |

| Economic Impact | Inflation and interest rates significantly influence pension payouts and plan health. |

| Maximizing Benefits | Understand plan documents and choose optimal payout options for your situation. |

| Advisor’s Role | Crucial for navigating complexities and integrating pensions into holistic financial plans. |

Frequently Asked Questions About 2026 Pension Updates

The main goals are to enhance the security and sustainability of defined benefit plans. This includes stricter funding requirements, improved transparency, and adaptation to evolving economic conditions and longer retiree lifespans, ensuring promises can be met.

Inflation can erode the purchasing power of fixed pension incomes. While some plans offer COLAs, they might not fully offset inflation. It’s crucial to understand your plan’s COLA provisions and consider supplementary income strategies.

This depends on your individual circumstances, health, and financial acumen. A lump sum offers flexibility but requires careful investment management, while an annuity provides predictable, lifelong income. Consulting a financial advisor is highly recommended for this critical decision.

You should thoroughly review your Summary Plan Description (SPD) and any annual benefit statements. These documents detail your eligibility, benefit calculation, vesting schedule, and available payout options. Request updated copies from your plan administrator.

A financial advisor can provide expert guidance on payout choices, analyze tax implications, and integrate your pension with your overall financial plan. They help ensure your pension works optimally within your complete retirement strategy, offering peace of mind.

Conclusion

The Pension Plan Updates 2026 represent a critical juncture for individuals relying on defined benefit plans for their retirement security. The evolving regulatory landscape, economic pressures, and demographic shifts all underscore the importance of proactive engagement and informed decision-making. By understanding your specific plan, staying abreast of legislative changes, and leveraging the expertise of financial professionals, you can navigate these complexities effectively. Ultimately, securing a comfortable and stable retirement in the coming years hinges on taking a vigilant and strategic approach to your defined benefit options.