Student Loan Forgiveness 2026: New Eligibility Criteria Announced

The Department of Education’s 2026 student loan forgiveness program introduces new eligibility criteria set to impact approximately 2 million borrowers, bringing significant financial relief and policy shifts.

The landscape of higher education finance is constantly evolving, and 2026 is poised to bring significant changes for millions of Americans. The Department of Education has announced crucial updates to the Student Loan Forgiveness Program 2026, introducing new eligibility criteria that are expected to affect approximately 2 million borrowers. These revisions aim to streamline the forgiveness process and address long-standing concerns about student debt, promising a fresh start for many.

Understanding the New Eligibility Criteria for 2026

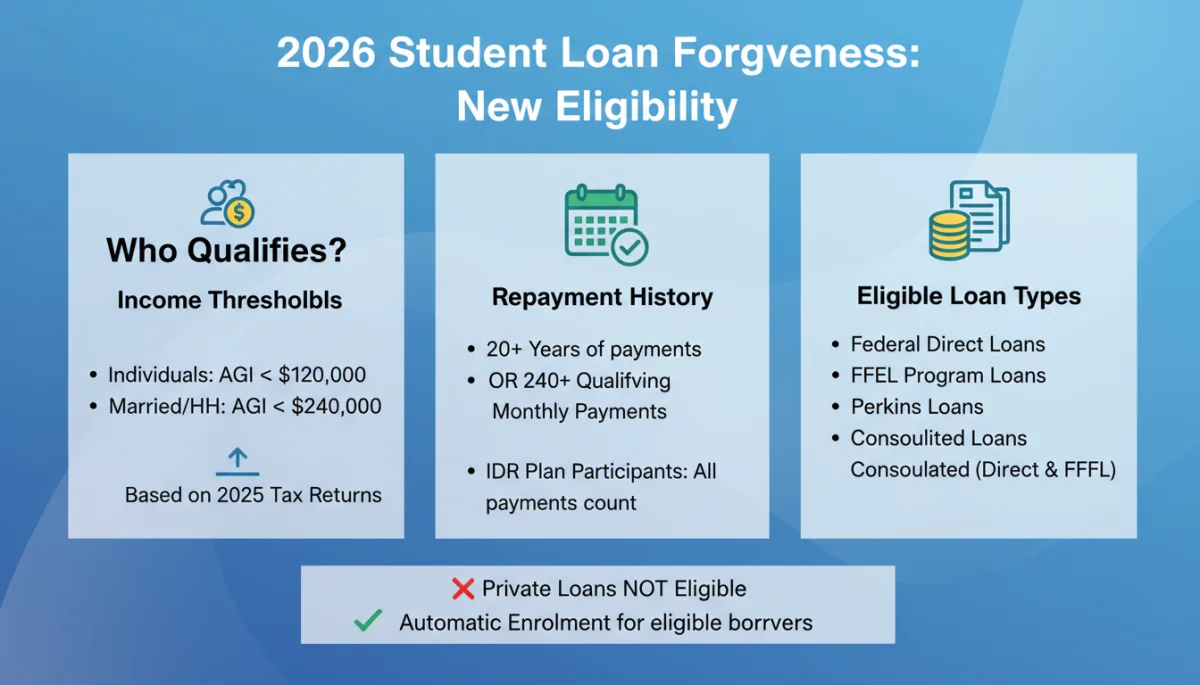

The core of the 2026 student loan forgiveness program lies in its updated eligibility criteria. These changes are designed to expand access to relief while ensuring the program remains fiscally responsible and targeted to those most in need. Borrowers should familiarize themselves with these new guidelines to determine their potential for forgiveness.

Income-Driven Repayment (IDR) Plan Adjustments

One of the most significant shifts involves the recalibration of Income-Driven Repayment (IDR) plans. The Department of Education has recognized that many borrowers on IDR plans have been making payments for decades without seeing a significant reduction in their principal balance. The new criteria seek to rectify this by offering accelerated forgiveness for certain long-term IDR participants.

- Borrowers who have made 20 years of qualifying payments on undergraduate loans, or 25 years on graduate loans, will now be eligible for automatic forgiveness, regardless of their remaining balance.

- The new rules also include a provision for a lower discretionary income percentage used to calculate monthly payments, making IDR plans more affordable for low-income borrowers.

- Periods of deferment and forbearance will now be reviewed more carefully, with some previously ineligible periods potentially counting towards forgiveness under specific circumstances.

Targeted Relief for Specific Loan Types and Professions

Beyond IDR, the program introduces more specific relief for certain loan types and individuals in public service or other critical professions. This targeted approach acknowledges the varying impacts of student debt across different sectors of the workforce and educational pathways.

- Federal Family Education Loan (FFEL) Program loans, previously excluded from some federal forgiveness initiatives, are now more comprehensively integrated into the 2026 program, allowing more FFEL borrowers to qualify.

- The Public Service Loan Forgiveness (PSLF) program has seen further simplification, with a clearer definition of qualifying employment and a more straightforward application process, aiming to reduce the historically high rejection rates.

- Borrowers in specific high-need professions, such as nursing, teaching in underserved areas, and certain medical fields, may find expedited pathways to forgiveness, recognizing their invaluable contributions to society.

These revised criteria represent a substantial effort to make student loan forgiveness more accessible and equitable. Understanding these nuances is the first step for borrowers hoping to benefit from the 2026 program.

Impact on 2 Million Borrowers: Who Benefits Most?

The Department of Education estimates that approximately 2 million borrowers will be directly impacted by these new eligibility criteria. This broad reach signifies a major policy shift intended to alleviate the burden of student debt for a substantial segment of the American population. Identifying who benefits most requires a closer look at the demographics and loan histories targeted by the program.

Long-Term Borrowers and IDR Participants

A significant portion of the beneficiaries will be long-term borrowers who have been diligently making payments under Income-Driven Repayment plans for many years. The automatic forgiveness after 20 or 25 years of payments on undergraduate or graduate loans, respectively, is a game-changer for these individuals. Many have faced the frustration of seeing their balances grow despite consistent payments due to interest accrual. This provision offers a definitive end to their debt journey.

Low-Income Individuals and Families

The adjustments to IDR payment calculations, which lower the percentage of discretionary income used, will disproportionately benefit low-income borrowers and their families. By reducing monthly payment burdens, the program aims to free up financial resources for essential needs, stimulating local economies and improving overall financial stability for vulnerable households. This is a crucial step towards addressing economic inequality exacerbated by student debt.

Public Service Professionals and FFEL Holders

Professionals in public service, including teachers, nurses, and government employees, will find the simplified PSLF program much more effective. The previous complexities and high denial rates often deterred eligible individuals. The enhanced clarity and streamlined process mean more dedicated public servants can achieve the forgiveness they were promised. Furthermore, the inclusion of more FFEL loans ensures that a wider array of borrowers, many of whom have older loans, can also access relief, closing a long-standing gap in federal forgiveness programs.

Overall, the program is designed to provide relief across various demographics, focusing on those who have demonstrated consistent efforts to repay their loans or who serve in critical public roles. The goal is to foster economic mobility and reduce financial stress, allowing millions to pursue their life goals without the crushing weight of student debt.

Recent Updates and Department of Education Announcements

The journey to the 2026 student loan forgiveness program has been marked by several key announcements and policy updates from the Department of Education. These recent developments provide crucial context and detail regarding the implementation and scope of the program, reflecting an ongoing commitment to refine and improve student debt relief initiatives.

Timeline for Implementation and Application

The Department of Education has outlined a clear timeline for the rollout of the new criteria. While the full program officially takes effect in 2026, many preparatory steps are already underway. Borrowers are advised to monitor official communications closely for specific dates regarding application windows and automatic forgiveness processing.

- Initial data reviews for automatic forgiveness eligibility under IDR adjustments are projected to begin in late 2025.

- A new, simplified application portal for PSLF and other targeted forgiveness programs is expected to launch in early 2026.

- Information sessions and outreach campaigns will be conducted throughout 2025 and 2026 to ensure borrowers are well-informed about the changes and how to apply.

Communication Strategies and Borrower Outreach

Recognizing past challenges with borrower awareness, the Department of Education is focusing on robust communication strategies. This includes direct outreach to potentially eligible borrowers, partnerships with financial aid offices, and transparent online resources. The aim is to prevent eligible individuals from missing out due to lack of information.

Official channels, such as the Federal Student Aid website and direct email campaigns, will be the primary sources of information. Borrowers should be wary of third-party solicitations and ensure they are accessing information from legitimate government sources to avoid scams. The Department emphasizes that there are no fees associated with applying for federal student loan forgiveness.

These continuous updates underscore the dynamic nature of student loan policy. Borrowers are encouraged to remain proactive in seeking information and verifying their eligibility as the program’s effective date approaches.

Financial Impact: What Borrowers Can Expect

The financial ramifications of the 2026 student loan forgiveness program are substantial, not only for individual borrowers but also for the broader economy. Understanding these impacts can help borrowers plan their financial futures and prepare for the changes ahead.

Direct Debt Relief and Savings

For the estimated 2 million borrowers who qualify, the most immediate and tangible benefit will be the direct reduction or elimination of their student loan debt. This translates into significant monthly savings, as borrowers will no longer be obligated to make payments. These savings can then be redirected towards other financial goals, such as saving for a home, retirement, or investing in their education or businesses.

- Elimination of monthly loan payments, freeing up hundreds or even thousands of dollars each month.

- Reduction in overall interest paid over the lifetime of the loan, especially for those with high balances.

- Improved credit scores for borrowers whose debt-to-income ratios decrease significantly, potentially leading to better terms on other loans.

Economic Ripple Effects

Beyond individual relief, the program is expected to have broader economic ripple effects. When millions of Americans have more disposable income, it can stimulate consumer spending, boost local economies, and even contribute to job creation. The reduction in household debt can also lead to increased financial stability across communities.

However, it is important to note that the program also entails significant government expenditure. The long-term economic impact will depend on how these costs are managed and offset. Policymakers are continually evaluating these factors to ensure the program’s sustainability and effectiveness.

Ultimately, for individual borrowers, the financial impact is overwhelmingly positive, offering a much-needed reprieve and the opportunity to build a more secure financial future. The program aims to re-energize a segment of the population previously constrained by overwhelming debt.

Comparing 2026 Forgiveness with Previous Programs

The 2026 student loan forgiveness program builds upon, and in some cases significantly departs from, previous federal student loan relief initiatives. A comparative analysis helps to highlight the unique aspects and improvements of the current program, offering a clearer picture of its potential effectiveness and reach.

Evolution of Forgiveness Policies

Historically, student loan forgiveness has been available through various, often complex, programs like PSLF, borrower defense to repayment, and specific IDR plans. However, these programs frequently faced criticism for their stringent requirements, lack of clarity, and low approval rates. The 2026 program appears to be a direct response to these shortcomings, aiming for greater simplicity and accessibility.

- Broader Eligibility: Unlike some previous programs that focused narrowly on specific cohorts or circumstances, the 2026 criteria cast a wider net, particularly with the enhanced IDR forgiveness and inclusion of FFEL loans.

- Streamlined Processes: Past forgiveness efforts were often mired in bureaucratic hurdles. The 2026 program emphasizes automatic forgiveness for eligible IDR participants and a simplified PSLF application, reducing administrative burdens for borrowers.

- Focus on Long-Term Debtors: A key distinction is the explicit focus on borrowers who have been in repayment for two decades or more, an area where previous programs often fell short in providing comprehensive relief.

Lessons Learned from Past Challenges

The Department of Education has clearly incorporated lessons learned from the challenges of prior forgiveness attempts. The high denial rates for PSLF, for instance, led to temporary waivers and now, a more permanent restructuring within the 2026 framework. Similarly, the complexities surrounding FFEL loan consolidation for forgiveness have been addressed to offer more direct pathways.

This iterative improvement indicates a commitment to creating a more effective and equitable system for student loan relief. While no program is perfect, the 2026 initiative represents a significant step forward in addressing the national student debt crisis with more practical and borrower-centric solutions.

Preparing for Student Loan Forgiveness 2026

As the 2026 student loan forgiveness program approaches, borrowers have several proactive steps they can take to prepare and maximize their chances of benefiting from the new eligibility criteria. Early preparation can significantly streamline the process and prevent potential setbacks.

Reviewing Your Loan History and Records

The first crucial step is to meticulously review your federal student loan history. This includes understanding your loan types (e.g., Direct Loans, FFEL loans), your repayment history, and any periods of deferment or forbearance. Accessing your account on the Federal Student Aid website (studentaid.gov) is the best starting point.

- Verify your loan servicers and ensure your contact information is up to date.

- Consolidate any FFEL Program loans into a Direct Consolidation Loan if you haven’t already, as this may be a prerequisite for certain forgiveness pathways under the new rules.

- Document all past payments and periods of enrollment or public service, as these records will be essential for verifying eligibility.

Staying Informed and Seeking Guidance

Given the dynamic nature of government programs, staying informed is paramount. Regularly check official Department of Education announcements and reputable financial aid news sources. If you have complex circumstances, consider seeking guidance from certified financial counselors or non-profit organizations specializing in student debt.

Avoid any services that charge a fee for student loan forgiveness assistance, as the process for federal programs is free. The Department of Education will never ask for payment to process your forgiveness application. Being vigilant against scams is an important aspect of preparation.

By taking these preparatory measures, borrowers can position themselves effectively to navigate the 2026 student loan forgiveness program and take full advantage of the relief it offers.

| Key Program Aspect | Brief Description |

|---|---|

| Eligibility Criteria | Expanded access for IDR long-term payers (20/25 years), simplified PSLF, and inclusion of more FFEL loans. |

| Affected Borrowers | Approximately 2 million borrowers, primarily long-term IDR participants, low-income individuals, and public servants. |

| Financial Impact | Direct debt relief, increased disposable income, potential credit score improvement, and broader economic stimulation. |

| Preparation Steps | Review loan history, update contact info, consider consolidation, and stay informed via official channels. |

Frequently Asked Questions About 2026 Loan Forgiveness

The program primarily targets long-term borrowers on Income-Driven Repayment plans, low-income individuals, and public service professionals. It also expands relief to certain Federal Family Education Loan (FFEL) program borrowers who previously had limited options.

No, the 2026 student loan forgiveness program, like most federal initiatives, applies exclusively to federal student loans. Private student loans are not eligible for forgiveness under these new Department of Education criteria.

Borrowers should review their federal loan history on studentaid.gov, ensure all contact information is current, and consider consolidating FFEL loans. Staying informed through official Department of Education announcements is also crucial.

Under current federal law, many forms of student loan forgiveness, particularly those related to IDR plans or PSLF, are not considered taxable income through 2025. Borrowers should consult a tax professional for the most up-to-date information regarding 2026 and beyond.

Official and most reliable information will be available directly from the U.S. Department of Education and the Federal Student Aid (FSA) website at studentaid.gov. Be cautious of unofficial sources and scams.

Conclusion

The Student Loan Forgiveness Program 2026 marks a pivotal moment in addressing the nation’s student debt crisis. With its expanded eligibility criteria and targeted relief for approximately 2 million borrowers, the Department of Education aims to provide substantial financial reprieve and foster greater economic stability. As the program rolls out, staying informed, reviewing personal loan histories, and utilizing official resources will be paramount for borrowers seeking to navigate these changes successfully. This initiative represents a significant step towards a more equitable and manageable future for millions burdened by educational debt.