2026 Home Equity Loans vs. HELOCs: Financing Major Expenses

Understanding the differences between home equity loans and Home Equity Lines of Credit (HELOCs) in 2026 is crucial for homeowners looking to finance significant expenditures, offering distinct approaches to leveraging home value.

Navigating financial decisions for major expenses in 2026 requires a clear understanding of your options. For many homeowners, leveraging their property’s value through home equity financing presents a powerful solution. This guide will delve into the nuances of 2026 Home Equity Loans vs. HELOCs: A Comparative Guide for Financing Major Expenses, helping you determine which path aligns best with your financial goals and needs.

understanding home equity: what it means in 2026

Home equity represents the portion of your property that you truly own, free and clear of mortgage debt. As property values continue to evolve and mortgage payments reduce your principal, your equity grows. In 2026, with a dynamic real estate market, understanding your available equity is the first step toward unlocking its potential for significant financial undertakings.

Calculating your home equity is straightforward: subtract your outstanding mortgage balance from your home’s current market value. Lenders typically allow you to borrow a percentage of this equity, often up to 80% or 85%, depending on various factors including your credit score and debt-to-income ratio. This accessible capital can be a game-changer for large-scale projects or unexpected costs.

the importance of accurate home valuation

- Professional appraisal: Lenders will require a recent appraisal to determine your home’s current market value accurately, ensuring a realistic assessment of your equity.

- Market trends: Local real estate market conditions in 2026 significantly influence valuations, so staying informed about neighborhood trends is beneficial.

- Property improvements: Recent upgrades or renovations can boost your home’s value, directly impacting the amount of equity you can access.

Knowing your precise equity allows you to approach lenders with confidence, understanding the maximum amount you might be eligible to borrow. This foundational knowledge is essential before diving into the specifics of home equity loans or HELOCs.

home equity loans in 2026: a fixed-rate solution

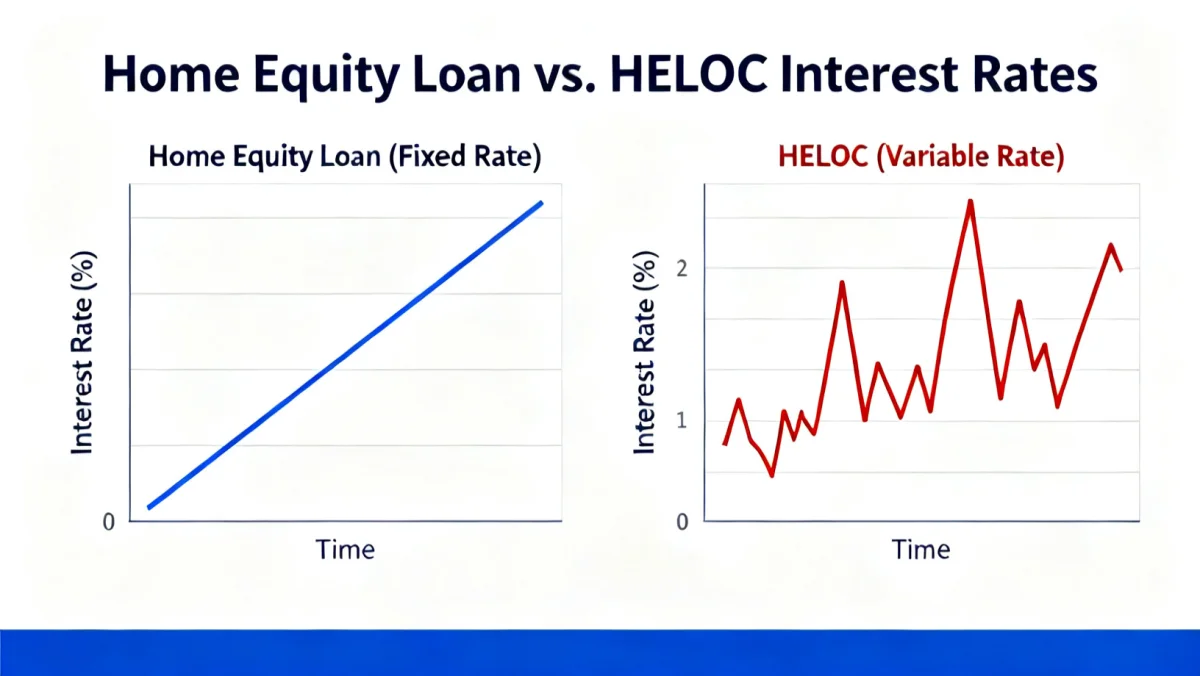

A home equity loan, often referred to as a "second mortgage," provides a lump sum of money upfront, which is then repaid over a fixed period with fixed monthly payments. This structure offers predictability, making it an attractive option for those who prefer stable budgeting and clear repayment schedules. In 2026, fixed interest rates can provide a sense of security against potential market fluctuations.

Borrowers typically receive the entire loan amount at closing, which is ideal for one-time, large expenses such as a major home renovation, consolidating high-interest debt, or funding a child’s education. The fixed interest rate means your monthly payments remain constant throughout the loan term, regardless of changes in the broader economic landscape.

predictable payments and budgeting

- Fixed interest rates: Your interest rate is locked in for the life of the loan, offering protection from rising rates.

- Consistent monthly payments: Simplify financial planning with an unchanging payment amount each month.

- Clear repayment term: Know exactly when your loan will be paid off, usually ranging from 5 to 30 years.

The fixed nature of home equity loans eliminates surprises, allowing homeowners to plan their finances meticulously. This stability is particularly appealing in an economic environment where interest rates might be volatile, providing a reliable financial anchor for significant investments.

helocs in 2026: flexible credit for ongoing needs

A Home Equity Line of Credit (HELOC) operates more like a credit card, allowing you to borrow money as needed, up to a pre-approved limit. This flexible borrowing option is characterized by a draw period, during which you can access funds, and a repayment period. In 2026, HELOCs remain a popular choice for homeowners needing ongoing access to funds without borrowing the full amount at once.

HELOCs typically come with variable interest rates, meaning your monthly payments can fluctuate based on market conditions. This flexibility can be advantageous if you anticipate needing funds intermittently for projects like phased renovations or managing irregular expenses. You only pay interest on the amount you actually borrow, not the entire credit line.

draw periods and repayment phases

- Draw period: Typically lasts 5-10 years, allowing you to borrow and repay funds multiple times within your credit limit.

- Variable interest rates: Payments can change, offering potential savings if rates fall, but also risk if they rise.

- Interest-only payments: Some HELOCs allow interest-only payments during the draw period, reducing initial financial strain.

The adaptability of a HELOC makes it suitable for evolving financial needs, providing a safety net for unforeseen expenses or a flexible funding source for projects that unfold over time. However, borrowers must be prepared for the potential for fluctuating payments due to variable interest rates.

key differences: interest rates, access, and repayment

The fundamental distinction between home equity loans and HELOCs lies in their interest rate structure, how funds are accessed, and their repayment mechanisms. Understanding these core differences is essential for making an informed decision that aligns with your financial strategy in 2026.

Home equity loans offer a predictable, fixed-rate environment, ideal for those who prefer stability. You receive a lump sum and repay it with consistent monthly payments. Conversely, HELOCs provide a variable rate and a revolving line of credit, offering flexibility for ongoing expenses but with the caveat of fluctuating payments.

comparing the core features

- Interest rate structure: Fixed for home equity loans, variable for HELOCs.

- Fund access: Lump sum for loans, revolving credit line for HELOCs.

- Repayment: Fixed monthly payments for loans, variable payments (often interest-only during draw period) for HELOCs.

The choice between the two often comes down to your personal financial comfort with risk, your need for immediate capital versus ongoing access, and your ability to manage potentially fluctuating monthly payments. Evaluating these aspects carefully will guide you towards the most suitable option.

when to choose a home equity loan in 2026

A home equity loan is often the preferred choice when you have a specific, large expense that requires a single, upfront disbursement of funds. In 2026, situations such as a major home renovation, debt consolidation, or a significant educational investment are prime examples where the stability of a fixed-rate loan is highly advantageous.

The predictability of fixed monthly payments and a defined repayment schedule offers peace of mind, allowing you to budget effectively without concerns about interest rate hikes impacting your financial outlay. This makes home equity loans an excellent tool for long-term financial planning where cost certainty is paramount.

ideal scenarios for home equity loans

- Large, one-time expenses: Perfect for a comprehensive kitchen remodel or a new roof where the total cost is known.

- Debt consolidation: Combining high-interest credit card debt into a lower, fixed-rate payment can save significant money over time.

- Tuition payments: Financing a college education with predictable payments can ease the financial burden over several years.

If your financial needs are clearly defined and you value the security of consistent payments, a home equity loan in 2026 offers a robust and straightforward solution to finance your major expenses without unexpected financial shifts.

when to choose a HELOC in 2026

A HELOC shines when your financial needs are ongoing or less defined, requiring access to funds over an extended period rather than a single lump sum. In the evolving economic landscape of 2026, this flexibility can be invaluable for projects like multi-phase home improvements, emergency funds, or managing fluctuating expenses.

The ability to draw funds as needed and only pay interest on the borrowed amount provides significant cost efficiency for intermittent expenses. However, the variable interest rate demands a degree of financial flexibility and awareness, as payments can change with market conditions.

best uses for a HELOC

- Phased renovations: Ideal for projects where costs are spread out over time, allowing you to draw funds as each phase begins.

- Emergency fund: A HELOC can serve as a readily available safety net for unforeseen financial emergencies, without incurring interest until used.

- Investment opportunities: Providing accessible capital for timely investments, allowing you to act quickly when opportunities arise.

For those who prioritize adaptability and prefer to manage their borrowing as their needs evolve, a HELOC in 2026 offers a powerful, dynamic financial tool. It empowers homeowners to maintain control over their borrowing, aligning expenses with immediate requirements.

factors to consider before deciding in 2026

Before committing to either a home equity loan or a HELOC in 2026, several critical factors warrant careful consideration. These include your current financial situation, future financial goals, and your comfort level with different types of interest rates and repayment structures. Making an informed decision requires a thorough personal assessment.

Consider the prevailing interest rate environment in 2026. If rates are low and expected to rise, a fixed-rate home equity loan might be more appealing. Conversely, if rates are high but anticipated to fall, a variable-rate HELOC could offer future savings. Your credit score and debt-to-income ratio will also significantly influence the terms you’re offered.

important considerations

- Interest rate outlook: Assess whether fixed or variable rates align with your predictions for the 2026 economic climate.

- Loan fees and closing costs: Both options come with fees; compare these to understand the total cost of borrowing.

- Impact on credit score: Understand how applying for and managing either loan type can affect your credit standing.

Ultimately, the best choice depends on your unique financial profile and the nature of the expenses you plan to finance. Consulting with a financial advisor can provide personalized insights, ensuring you select the option that best supports your long-term financial health and goals in 2026.

| Feature | Description |

|---|---|

| Interest Rate Type | Home Equity Loans typically have fixed rates; HELOCs have variable rates. |

| Fund Access | Lump sum for loans; revolving credit line for HELOCs. |

| Repayment Structure | Fixed monthly payments for loans; variable payments for HELOCs. |

| Best Use Case | Loans for defined, one-time expenses; HELOCs for ongoing, flexible needs. |

frequently asked questions about home equity financing in 2026

The main difference lies in how funds are disbursed and repaid. A home equity loan provides a lump sum with a fixed interest rate and fixed payments, while a HELOC is a revolving credit line with a variable interest rate and flexible draws, similar to a credit card.

Generally, yes. Home equity funds can be used for various purposes, including home improvements, debt consolidation, education expenses, or other significant purchases. Lenders typically do not restrict the use of the funds once they are disbursed.

Under current tax laws, interest paid on home equity loans and HELOCs may be tax-deductible if the funds are used to buy, build, or substantially improve the home that secures the loan. It’s always advisable to consult a tax professional for personalized advice.

If home values decline significantly, your lender may reduce your available credit line or even freeze it. This is because the credit line is secured by your home’s equity, and a drop in value increases the lender’s risk. This is known as a "margin call" or "credit line reduction."

A strong credit score is crucial for securing favorable terms and interest rates for both home equity loans and HELOCs. Lenders use your credit score to assess your creditworthiness and your ability to repay the loan, influencing approval and borrowing costs.

conclusion

Choosing between a home equity loan and a HELOC in 2026 is a significant financial decision that hinges on your specific needs and comfort with risk. Whether you require a predictable lump sum for a defined expense or flexible access to funds for ongoing projects, understanding the distinct characteristics of each option is paramount. By carefully evaluating interest rates, repayment structures, and your personal financial situation, you can leverage your home’s equity effectively to finance your major expenses and achieve your financial aspirations with confidence and clarity.